Banks have to Act: The EU is redefining how instant payments are handled

Instant Payment Screening

Financial Institutions/FinTech

Blog

The EU is accelerating the rollout of instant payments. Since January 9, 2025, payment service providers (PSP) have been required to receive instant payments (IP). As of October 9, 2025, they must also be able to send them. In Switzerland, instant payments have been mandatory for around 70 major financial institutions since August 20, 2024. Additional institutions are expected to follow in 2026.

Implementing the Instant Payment Regulation presents significant challenges for banks and PSPs – particularly with regard to sanctions screening.

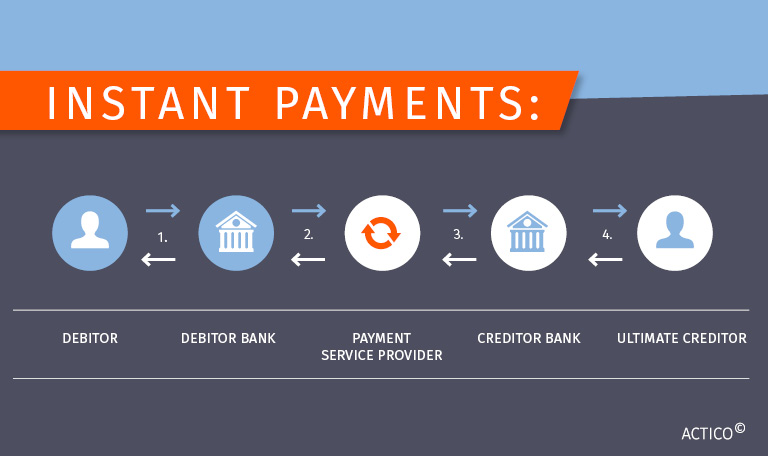

The Difference Between instant payments and standard credit transfers

Instant payments, also known as SEPA instant credit transfers (SCT Inst), are Euro transfers within the 34 countries of the Single Euro Payments Area. These transactions enable the transfer of funds within 10 seconds – anytime, around the clock and 365 days a year. While instant payments are processed within ten seconds, standard transfers can take one or more days to complete.

Sanctions screening for instant payments

Payment service providers in the EU and beyond are now required to execute instant payments. However, determining how these transactions should be screened against sanctions lists is not always straightforward.

To meet the needs of bank customers who have to make funds immediately available to recipients, many banks offer instant payments, but only some of them extend the scope to include incoming payments too.

Payment service providers such as banks, which provide standard credit transfers in euros, are required to offer the service of sending and receiving instant payments in euros.

The charges must not be higher than the charges that apply for standard credit transfers.

Deadlines for implementation:

Receive instant credit transfers in euros: by 9 January 2025,

Send instant credit transfers in euros: by 9 October 2025

After this, for bank-PSPs in non-eurozone member states, the deadline for receiving instant payments is 9 January 2027, sending instant payments 9 July 2027.

The implications for instant payment customer screening

Under the new rules, PSPs need to verify that the beneficiary’s IBAN and name match in order to alert the payer to possible mistakes or fraud before a transaction is made.

PSPs should periodically, and at least daily, verify whether their Payment Service Users (PSUs) are persons or entities subject to targeted financial restrictive measures, and should no longer apply transaction-based screening in that specific context.

The critical importance of robust customer screening in the era of Instant Payments: Discover more here

The obligation of PSPs to periodically verify their PSUs is related only to persons or entities subject to targeted financial restrictive measures. Other types of restrictive measures adopted in accordance with Article 215 TFEU (Treaty on the Functioning of the European Union) or restrictive measures that are not adopted in accordance with Article 215 TFEU fall outside the scope of that obligation. The obligation of PSPs to periodically verify whether their PSUs are persons or entities subject to targeted financial restrictive measures does not interfere with actions that PSPs should be able to take to comply with EU law on the prevention of money laundering and terrorist financing.

Financial institutions operating in multiple countries or regions, decide which payments to examine depending on the regulatory context and their risk appetite. Relevant factors here include the type of payment (domestic vs. international), unusual patterns (e.g. pass-through transactions), transaction value and the payment’s origin/destination (e.g. country/region, recipient type).

Transaction based screening has to be conducted before the payment is executed. But since sanctions lists screening comprises just one part of the payment process, only a limited timeframe – between 500 milliseconds and one second – is available. A window this tight requires efficient IT infrastructure and bringing all available technical solutions into play, such as interface adjustments, storage of hits and clarifications, cache optimisation and workflow and GUI adaptations.

How are banks handling the instant payment obligation?

Banks having rolled out instant payment projects report needing a lead time of around half a year for analyses, bringing various areas on board and clarifying IT infrastructure.

Questions like these are quite likely to come up along the way:

How should the payment and compliance systems change to ensure 24/7 year-round availability?

What are the best interfaces for addressing peripheral systems?

How will requirements engineering be handled, in-house or with a service provider?

What is the core business? Are there opportunities to complement the business model?

What do customers expect?

What is the risk of customer satisfaction deteriorating?

Beyond instant payments, can any other services be improved?

The goal: Opening up availability of Euro instant payments EU-wide

Execution of a real-time transfer requires payment service providers (PSPs) adhering to the same rules, practices, and standards (“Scheme”) to be present on both sides of the transaction. In 2017, the European Payment Council introduced the Single Credit Transfer (SCTInst) Scheme for Euro instant payments within SEPA. Broad participation by PSPs in this scheme is an essential prerequisite for the wide availability of Euro instant payments throughout the EU.

Instant payments in Switzerland: How and when?

The payments regulator in Switzerland, the Swiss National Bank, has created an obligation for financial institutions to participate in IP:

From August 2024 for larger banks

End of 2026 for the remaining banks

During the initial phase, the limit is CHF 20.000,–

Swiss instant payments went live on 20 August, 2024, meaning that individuals and companies can initiate account-to-account transactions. Swiss banks are not obligated to offer outgoing instant payments. Unlike the EU regulation, the Swiss regulation does not impose equivalent charges for standard transfers and instant payments.

The Swiss Interbank Clearing (SIC) payment system, operated by SIX on behalf of the Swiss National Bank, connects bank accounts. Technically, SIC is capable of processing real-time payments. However, to make Instant Payments work across the entire payment chain, adjustments are needed in both the operation and organisation of interfaces between banks and SIX. With the launch of the fifth generation of SIC at the end of 2023, SIX laid the foundation for instant payments, similar to the European SEPA Instant Credit Transfer standard.

The six key questions to ask on instant payment and sanctions screening:

How is system availability defined?

A 24/7 round-the-clock service year-round, with zero downtime

What is the maximum tolerable response time?

A maximum of 10 seconds

What does this mean in the context of sanctions screening?

PSPs should periodically, and at least daily, verify whether their PSUs are persons or entities subject to targeted financial restrictive measures, and should no longer apply transaction-based screening in that specific context. However, they must comply with Union law on AML and CFT.

Which data does the sanctions screening check for instant payments?

The sanctions screening checks transaction data, such as IBAN, purpose of use, blocked banks or countries.

What is the difference between screening of standard bank transfers?

The instant payment screening function compares remittance data with sanctions and blacklists and as soon as a “hit” is found, the payment is rejected. Unlike standard bank transfers, instant payments do not allow for manual intervention during processing. To keep customer satisfaction high, it becomes even more crucial to reduce false positives via screening of instant payments than with SEPA credit transfers.

What role must an IT system fill in instant payment screening?

Instant payment screening and the need to perform the checking mentioned within 500 milliseconds and no more than a second has a massive impact on the IT infrastructure and requires interface adjustments. The storage of hits and clarifications must also be adapted to the strict time regime and the cache, workflow and GUI all have to be further optimised.

Summary

In March 2024 the EU published a regulation that makes instant payments fully available in euros to consumers and businesses in the EU and EEA countries. The new rules came into force on 9 January 9 2025 for incoming IP. Sending instant payments will be mandatory by 9 October 2025.

The Swiss National Bank wants to do all that is needed for instant payment to become the new normal in Switzerland. This required the expansion of the technical infrastructure and the participation of the banks in the new process. Since August 20, 2024, Swiss banks are able to receive instant payments from other Swiss banks. Smaller banks which process less than 500,000 transfers per year have until the end of 2026 to get set up.

For bank-PSPs in non-eurozone member states, the deadline for receiving instant payments is 9 January 2027, sending instant payments 9 July 2027.

Customer screening has taken on new urgency with instant payments. Daily checks of customer data against sanctions lists bring unique challenges. Explore the key challenges banks are tackling in this article.

You are currently viewing a placeholder content from Hubspot Embedded Content. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

You are currently viewing a placeholder content from Hubspot Meetings. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

You are currently viewing a placeholder content from Wistia. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.