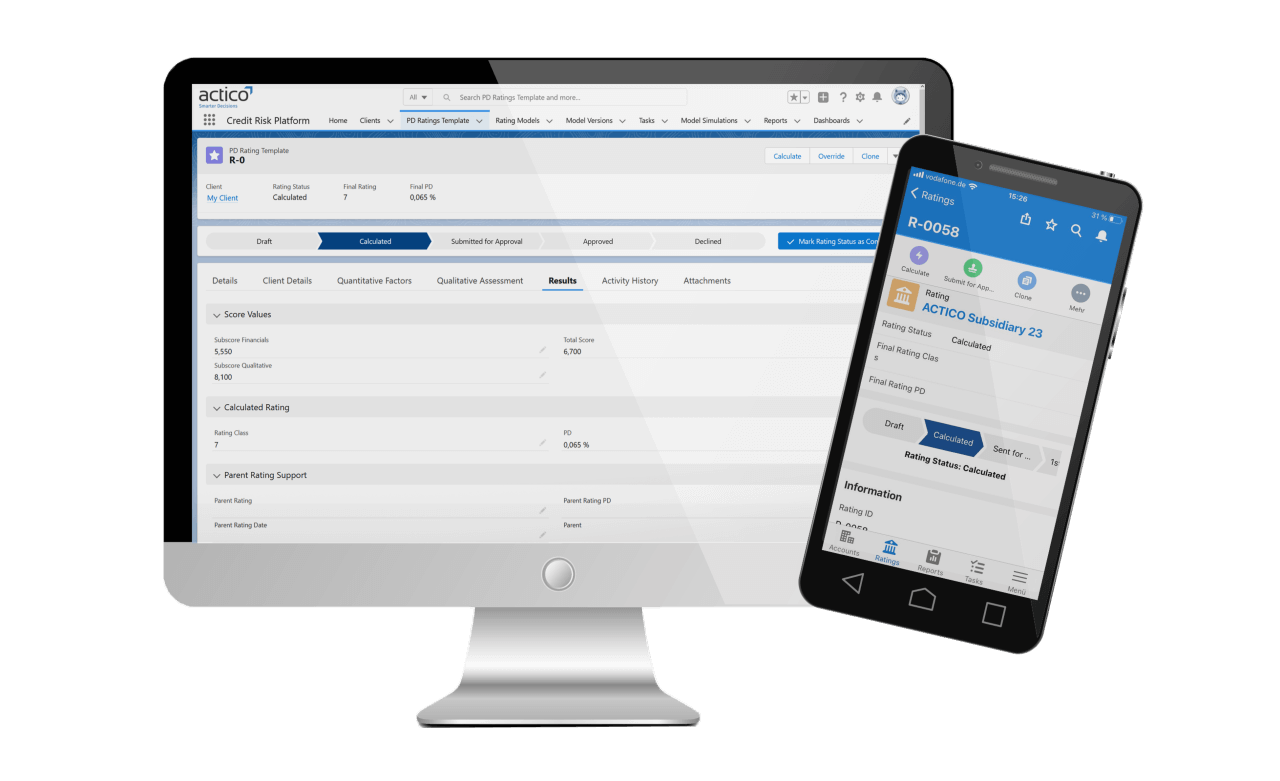

“ACTICO provides the bank with an integrated system for all rating models that comprehensively supports our credit analysts during the rating workflow.”

Dr. Stefan Krohnsnest

Head of Risk Controlling, DZ Hyp

Evaluate, manage, and minimise potential credit risks while streamlining your decision-making processes. Explore the Credit Risk Management Software from ACTICO.

Credit risk management is, and will remain, the focus of intense regulatory scrutiny. To comply with stricter regulatory requirements, credit institutions overhaul their credit risk management approaches. Yet, viewing this as merely a compliance exercise is short-sighted. Improved credit risk management fulfils regulatory requirements and provides an opportunity to improve overall performance and secure a competitive advantage.

Banks must implement an integrated, quantitative and qualitative credit risk solution to reduce loan losses and ensure that capital reserves accurately reflect the risk profile. The solution should enable banks to get up and running quickly with straightforward portfolio measures and also provide a path to more advanced credit risk management measures as needs change.

Agentic AI marks the next evolution beyond Generative AI. Instead of executing single prompts, agents autonomously perform complete tasks – from data collection to analysis. For credit risk teams, this means fewer manual steps, faster decisions, and greater consistency.

Discover in this Business Insight how Agentic AI transforms credit risk workflows and what prerequisites are key for its use in regulated environments.

“ACTICO provides the bank with an integrated system for all rating models that comprehensively supports our credit analysts during the rating workflow.”

Dr. Stefan Krohnsnest

Head of Risk Controlling, DZ Hyp

Take control of credit risk, compliance requirements and regulatory demands. Enjoy the flexibility and scalability of features like real-time risk model updates, user permission controls and seamless connections to your internal and third party systems.

Start the digital transformation of your credit risk management now!

ACTICO is designed to meet the specific demands of your market, business, and customer needs. It addresses current industry-specific issues while being adaptable to future challenges.

ACTICO empowers your team with a user-friendly, drag-and-drop tool that eliminates the need for coding, offers flexibility, and sets industry standards – regardless of the industry you are in. A credit risk decision-making software that is tailored to manage your risks – not those of others.

For many years, ACTICO has been recognised by customers and analysts as a leading provider of Advanced Decision Automation Technology and solutions for Compliance and Credit Risk Management.

You may also be interested in:

Live Event

Association of Bank Compliance Officers to Meet in the Philippines

Meet ACTICO at the ABCOMP Annual Conference 2026, Aug 10, The Peninsula Manila. See how AI-powered compliance keeps Philippine banks audit-ready.

Compliance

Financial Institutions/FinTech

AI

News

ACTICO Introduces Agentic AI for Decision Management: Agents Build the Decision Logic, Experts Approve

AI agents help teams build, test and document explainable decision logic faster while experts remain fully in control of every change.

Advanced Decision Automation

AI

Landing Page

Agentic AI in Decision Management

New agentic AI capabilities for your Decision Management: AI agents build, review and document decision logic at the speed and reach of AI, up to 65 percent faster. Every change is reviewed and approved by your business experts before it reaches production.

Credit Decisions, Retail Credit Decisioning

AI

Live Event

FinCrime Leaders Summit 2026: Let’s Talk AI in Compliance

Register for the FinCrime Leaders Summit 2026 in Frankfurt. Connect with compliance professionals and join the panel discussion on the role of AI.

Compliance

Financial Institutions/FinTech

AI

Newsletter

Regular News and Updates

Decision Management Platform

Compliance

Resources

You are currently viewing a placeholder content from Hubspot Embedded Content. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Hubspot Meetings. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Wistia. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information