Brochure

Deadline 10 July 2027: The EU AML Package Hits Insurers Hard

Anti-money laundering in insurance must change significantly due to the EU AML package: fewer manual processes, more automation.

Anti-Money Laundering

Insurance

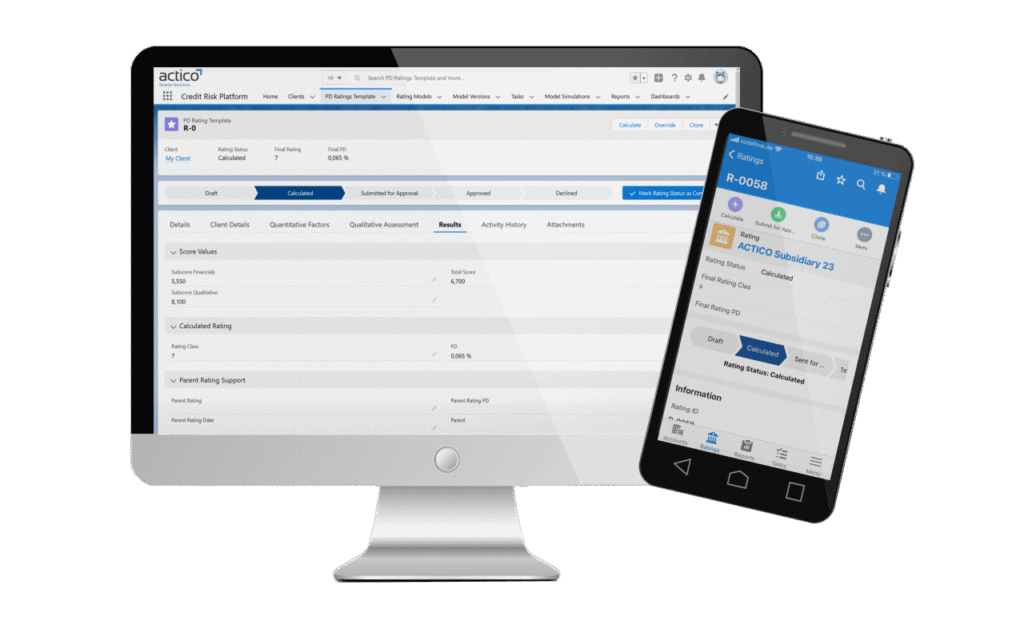

The risk rating models of our bank are IRB-compliant. Do I need to adapt the models or require approval by the regulators when using a new software platform?

No, we can replicate the existing rating model / logic in the new system. Using a powerful regression testing capability, we can verify that the new rating system delivers the same restults. The Credit Risk Platform has a comprehensive features-set to ensure the auditability and security of the rating system.

How does ACTICO handle the migration of risk rating data?

We support the data migration of historical data, such as risk ratings, financial spreads using a data migration tool which is agnostic to the legacy system in place.

How are the bank’s existing risk rating models integrated?

The models can be implemented using a graphical, no-code editor. Model changes are subject to a comprehensive audit trail and versioning concept. Alternatively, it is also possible to integrated pre-existing models, e.g. models which exist in Python and/or R.

What are technical possibilities to connect to existing risk rating systems?

The Credit Risk Platform can be seamlessly and bi-directionally integrated with a bank’s existing on-premise and cloud-based systems.

What is a typical time frame for a migration?

The time frame for migrating is dependent on various factors such as the number and complexity of rating models, reporting requirements, and integrations with internal or external systems. Please contact us to discuss your specific requirements and timelines for a possible system migration.

For many years, ACTICO has been recognised by customers and analysts as a leading provider of Advanced Decision Automation Technology and solutions for Compliance and Credit Risk Management.

You may also be interested in:

Brochure

Deadline 10 July 2027: The EU AML Package Hits Insurers Hard

Anti-money laundering in insurance must change significantly due to the EU AML package: fewer manual processes, more automation.

Anti-Money Laundering

Insurance

Webinar On-Demand

Anti-Money Laundering in Life Insurance: The EU AML Package is Coming. 2027 Is Closer Than You Think.

Why must life insurers fundamentally strengthen their anti-money laundering framework from 2027? The EU AML Package requires more robust IT systems. Watch the webinar.

Anti-Money Laundering

Financial Institutions/FinTech

Webinar On-Demand

Agentic AI in Action: How AI Agents Are Redefining Key Processes in Banking and Financial Services

Watch the Webinar to explore real-world agentic AI use cases in banking and financial services — plus a focused deep dive into commercial credit risk assessment with a live demo and sample ROI calculation.

Credit Risk Management

AI

Blog

FIU Reporting: Why Compliance Teams Are Getting Nervous – and How GenAI Can Help

FIUs and Switzerland’s MROS require financial institutions to submit SARs via goAML — they do not tolerate incomplete or delayed reports.

Financial Institutions/FinTech

Newsletter

Regular News and Updates

Decision Management Platform

Compliance

Resources

You are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Hubspot Meetings. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Wistia. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information