When Would You Use a Rule Engine?

Rule-based engines are essential to processing large amounts of customer transactions in the shortest time possible. Typical scenarios for rule engine application include:

- Automated compliance checks that should be reused in various processes and applications

- Pricing scenarios, e.g., multi-channel pricing, risk-based pricing, corporate pricing

- Risk assessment procedures, e.g., in insurance underwriting and claims processes

- Process automation scenarios with high requirements towards flexibility

- Digital transformation projects with multi-channel scenarios

- Validity reviews, validations, and centralized calculations

Rule-based engines are part of a company’s Business Rules Management System (BRMS) and are a good fit for complex, ever-changing business decisions.

How Do You Make a Rule Engine?

It’s possible to develop your rule-based engine since the development tools are easily accessible. However, due to the high volume of transactions and fast scalability of tech companies, it’s time-consuming and costly to do because it takes your team’s focus away from the core business. Therefore, it’s much more efficient to rely on an experienced partner who has developed an engine that fulfills the essential criteria.

Rule engines also differ in how the rules are added to the system. Some systems input rules using excel tables or with a graphical editor. An easy-to-use interface allows non-IT employees to add and change rules without needing IT’s assistance.

How Do You Write a Business Rule?

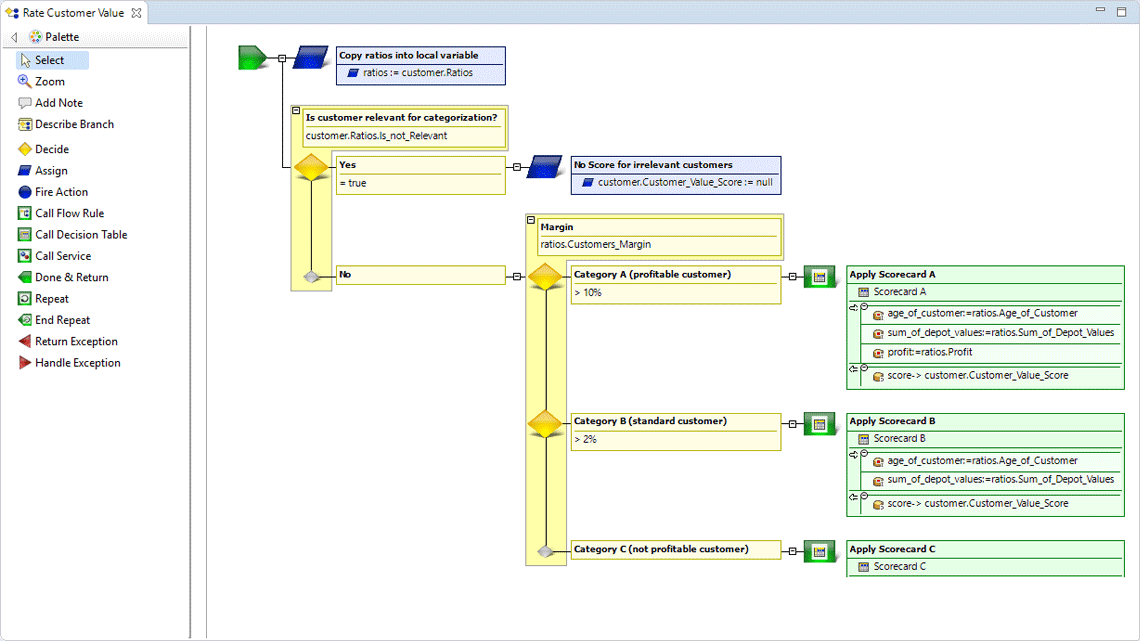

A business rule is a flowchart with queries, statements, and function calls created using a (graphical) editor as shown in the image below:

Information is collected in the form of rules and stored in a database. The engine picks rules according to conditions set and runs them based on the queries provided. If the rules match the requirements, then the engine executes the corresponding action and returns a solution.

In the image above, the rule-based engine queries the “Customers. Margin” variable and selects different actions depending on the variable’s value, such as applying a specific scorecard. The elements of this decision model can be assembled by mouse and customized by double-click.

Instead of just reading the content of a specific variable, a machine learning component can be queried to determine the probability that the customer will repay his loan on time. Depending on the result, the rule then performs various actions.

In the ACTICO Platform, business users create rules by dragging the elements of a business rule from a list to the work plane, linking them to existing features, and customizing the elements via detail settings. To do this, they enter assignments to variables or define threshold values for branching. Alternatively, rules are also described as decision tables. These allow different cases to be managed very compactly and clearly.

What Is the BRMS Tool?

A Business Rules Management System (BRMS) tool is a software application used to define, deploy, execute, monitor, and manage business rules and decision logic. A BRMS automates business rules and decision-making in an organization’s business processes. In addition, it can link different technology solutions to perform the required functions.

The BRMS consists of:

- A rule repository that stores and avails all defined rules whenever they’re needed

- A development environment with a (graphical) editor that even non-IT developers can work with

- A runtime environment that executes the set of rules with high performance (this is the actual business rule engine)

- Multiple interfaces to connect to the existing software applications in the Company

Many applications have all their business logic within the program’s code, making maintenance, analysis, and optimization complicated, time-consuming, and cost-intensive. In addition, this setup makes the rapid implementation of changes nearly impossible.

A BRMS helps companies to separate their rule-based business logic from the rest of the application’s logic. This separation gives non-IT users capabilities to model, maintain, and optimize the business rules logic and make changes without interfering with the application’s processes.

Users can then test the rules by creating input values as test cases, specifying the expected results, and executing the rules. If the results do not match the specifications, users can easily trace the execution of the rule and thus find and fix the reason for the deviation.

What Are Business Rules in Programming?

A business rule is a set of conditions that define specific actions within a business context. For example, in programming, a business rule refers to the portion of your application that represents the core functionality of your application and how it works.

Often confused with business logic, the two differ because business logic is responsible for encoding business rules into the software program. In contrast, the business rule asserts and defines the constraints, processes, or operations that apply to a company.

Business rules are formally written as policies or informal practices kept among employees and only known through verbal interactions.

The best practice is to document business rules to improve communication, legal compliance and ensure uniformity with information shared across the organization.