“We were looking for a robust and centralised platform to manage our internal rating models.”

James Berrecloth

Head of Risk Infrastructure, Santander UK

Banks and financial institutions are investing significant resources in the development and validation of internal models to assess credit risk, from Probability of Default (PD) models to Loss Given Default (LGD) models, to comply with IRB approaches and IFRS 9. ACTICO’s internal ratings platform software lets banks and financial service providers deploy and integrate these models in a flexible, workflow-enabled, fully-auditable borrower risk rating application, without lengthy IT implementation projects.

“We were looking for a robust and centralised platform to manage our internal rating models.”

James Berrecloth

Head of Risk Infrastructure, Santander UK

What is a Probability of Default (PD) model, and does ACTICO’s platform support it?

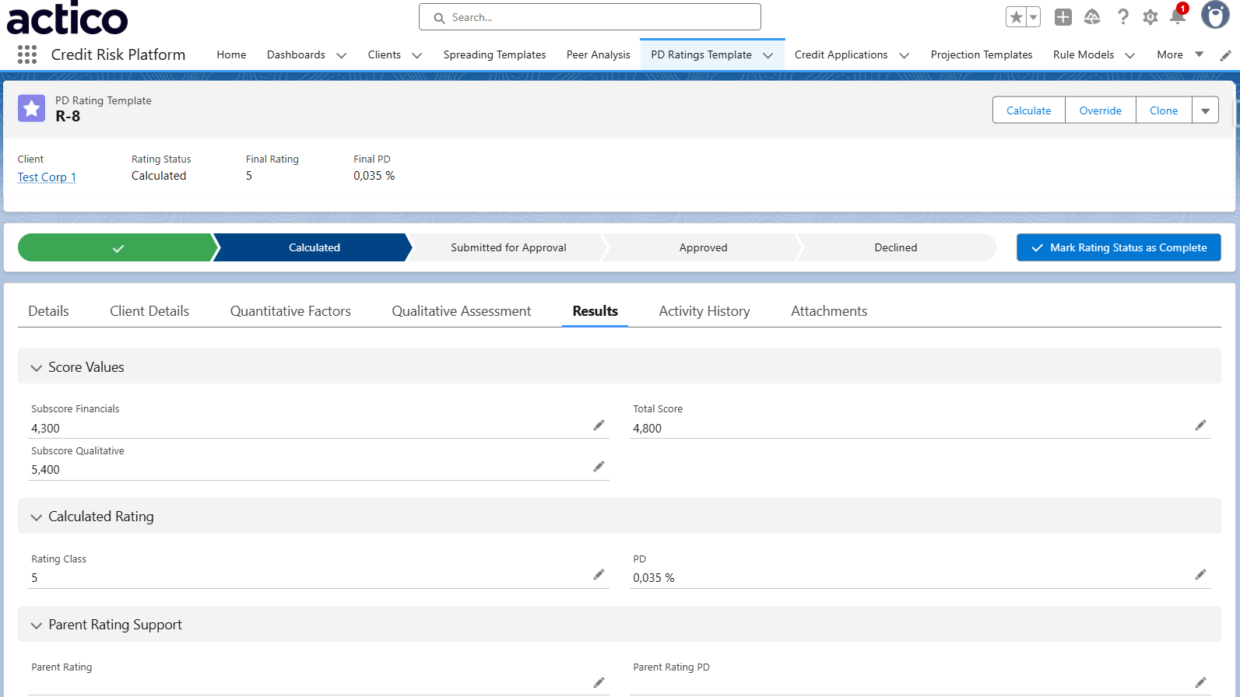

A Probability of Default (PD) model estimates the likelihood that a borrower will fail to meet their debt obligations over a defined time horizon — typically one year. PD models are a core component of credit risk management under Basel IRB frameworks and IFRS 9 expected credit loss (ECL) calculations. Banks typically maintain multiple PD models for different borrower segments: corporate obligors, SME borrowers, financial institutions, and retail clients.

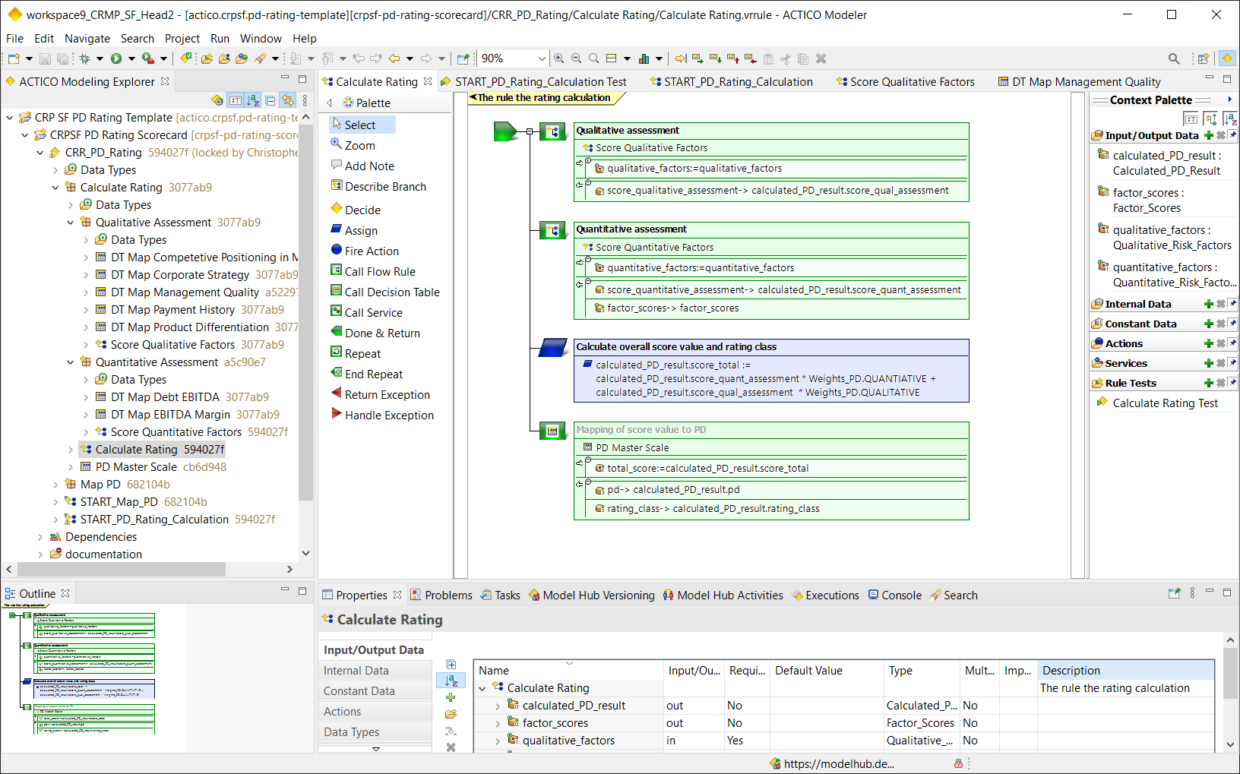

ACTICO’s Credit Risk Platform gives credit risk teams a graphical, no-code environment to configure, test, and deploy PD rating models. Whether your PD model is a statistical scorecard, an expert judgement-based rating system, or a hybrid combining financial ratios with qualitative overlays, the platform handles the full model lifecycle — from initial build and validation through to production deployment and ongoing monitoring.

What is a Loss Given Default (LGD) model, and is it supported on the same platform?

A Loss Given Default (LGD) model estimates the share of an exposure that a lender expects to lose in the event of a borrower default — after accounting for collateral recovery, workout costs, and the time value of money. LGD models operate at the facility level.

ACTICO’s Credit Risk Platform supports the implementation of both regulatory LGD estimates (for IRB approaches) and accounting LGD values (for IFRS 9 stage-specific loss calculations) — on the same centralized platform as your PD models, with full versioning, governance, and workflow capabilities.

Can we run both PD and LGD models on a single platform?

Yes. ACTICO’s Credit Risk Platform is designed as one centralized internal ratings platform for both PD and LGD models — as well as any other internal credit risk models your institution maintains. This eliminates the need for separate tooling across model types, reduces operational complexity, and ensures consistent governance and audit trails across your entire model portfolio.

Our models are implemented in Python and/or SAS. Do we need to re-implement our models?

No. The platform integrates seamlessly with existing model logic in other languages. Quantitative risk teams can continue working in their preferred modelling environment, while front-office analysts interact through a clean, web-based interface. There is no need for a lengthy reimplementation of the models.

How does the credit risk platform support banks in fulfilling regulatory requirements?

The platform is built to support the requirements of Basel IRB approaches and IFRS 9 expected credit loss calculations. This includes both regulatory capital estimates (e.g., IRB-compliant PD and LGD) and accounting-based estimates used in stage-specific IFRS 9 loss calculations. Full audit trails, model versioning, and role-based access controls are built in to support model governance requirements under these frameworks.

Can we test model changes before deploying them to production?

Yes. The platform includes simulation capabilities that allow teams to test proposed changes to PD, LGD, or other internal rating models against historical portfolios before go-live. This includes rating transition matrices and portfolio-level impact analysis — helping minimize model risk ahead of any new model release.

How does the platform handle model governance and versioning?

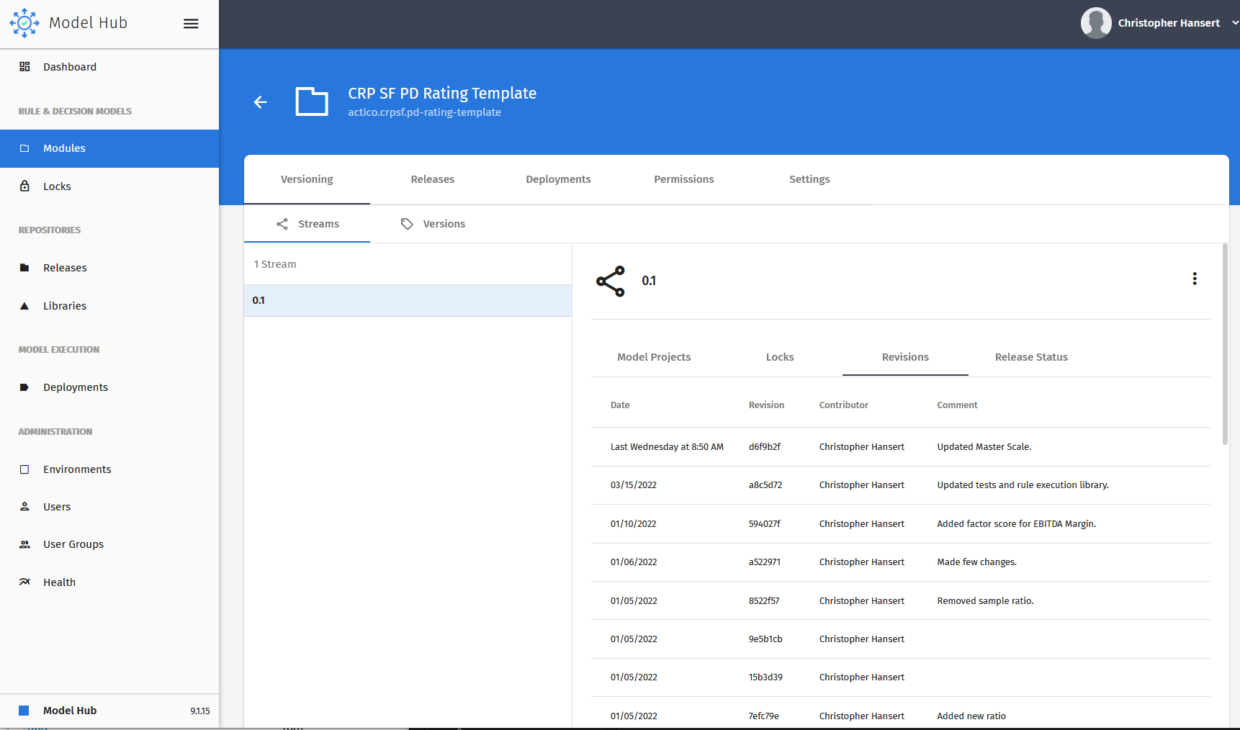

The platform uses a GIT-based central repository to store and manage all model versions, with full tracking of changes including timestamps and user IDs. Teams can create branches, tag versions, graphically compare model versions, and manage release and deployment workflows, with role-based and team-based access controls throughout.

Is the platform suitable for both credit risk teams and business/front-office users?

Yes. The platform is designed for both audiences. Risk model administrators use the graphical drag-and-drop modeler to configure and maintain rating models. Front-office analysts and relationship managers interact through a powerful, user-friendly web interface to capture qualitative and quantitative risk factors, submit ratings for approval, and manage their task lists.

For many years, ACTICO has been recognised by customers and analysts as a leading provider of Advanced Decision Automation Technology and solutions for Compliance and Credit Risk Management.

You may also be interested in:

Blog

How Compliance Views AI Agents, LLMs, and Data Sovereignty

Compliance in banking and insurance is embracing AI agents, LLMs, and the cloud, with costs and data sovereignty as key decision factors.

Compliance

AI

Live Event

Shaping the Future of Credit Decisioning – meet ACTICO in Manila

ACTICO joins the Annual Convention of Thrift Banks Philippines 2026 as Silver Sponsor. Discover how thrift banks are automating credit decisions at scale.

Credit Risk Management

Webinar

Webinar: Automated Financial Spreading – The Role of LLMs, Governance, and Audit Trails

Join this 30-minute webinar to understand why orchestrating multiple LLMs falls short on accuracy, auditability, and scale — and see a live demo of purpose-built decisioning AI in action.

Financial Spreading

AI

Thought Leadership

Agentic AI in Commercial Credit Risk | Accenture & ACTICO

How leading banks are deploying Agentic AI in commercial credit risk with the ACTICO Credit Risk Platform — insights from Accenture and ACTICO’s joint webinar. Download the Executive Briefing.

Credit Risk Management

AI

Newsletter

Regular News and Updates

Decision Management Platform

Compliance

Resources

You are currently viewing a placeholder content from Hubspot Embedded Content. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Hubspot Meetings. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Wistia. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information