News

ACTICO Expands Its Portfolio: Fact Integration Strengthens Market Position

Keensight Capital, one of the leading private equity managers dedicated to pan-European Growth Buyout investments, has acquired a majority stake in the ACTICO Group.

08.05.2025|

Changes to AML regulations in Switzerland have been introduced over recent years through different laws and international agreements:

ANTI-MONEY LAUNDERING & MACHINE LEARNING

ACTICO Anti Money Laundering is the Next Generation software to flag or detect conspicuous payments, behavioural patterns and customer relationships. It helps banks, insurers and financial services providers ensure AML compliance, automatically check customers, business relationships and transactions, and recognise potential money laundering.

The volume of incoming SARs continued to increase in 2024: Financial intermediaries sent MROS (Swiss Money Laundering Reporting Office) a total of 15,141 suspicious activity reports (SARs). This represents an increase of 27.5% compared with the previous year (2023: 11,876). On average, MROS received 59 SARs per working day. 92,3 per cent of money laundering reports in 2024 came from the financial sector.

The fourth FATF Enhanced Follow-up Report published in October 2023 analyses the progress assessed to remedy some of the technical compliance shortcomings identified in its MER. Eight of the 40 recommendations are now marked as “compliant” (C). 29 as largely compliant (PC). Three recommendations are classified as “partially compliant” (PC).

In October 2024, the FATF concluded the fourth round of mutual country evaluations. This peer-to-peer evaluation analysed the measures taken by over 200 member countries to tackle financial crime, terrorist financing and proliferation. The Mutual Evaluation Reports (MER) analyse the respective progress made by each country, but also reveal their weaknesses.

With the start of the 5th round of evaluations, Switzerland and thus MROS also began the preparatory work for the evaluation of Switzerland. The State Secretariat for International Finance (SIF) has the lead in coordinating these activities.

The next FATF mutual evaluation of Switzerland is expected to take place in 2027/2028.

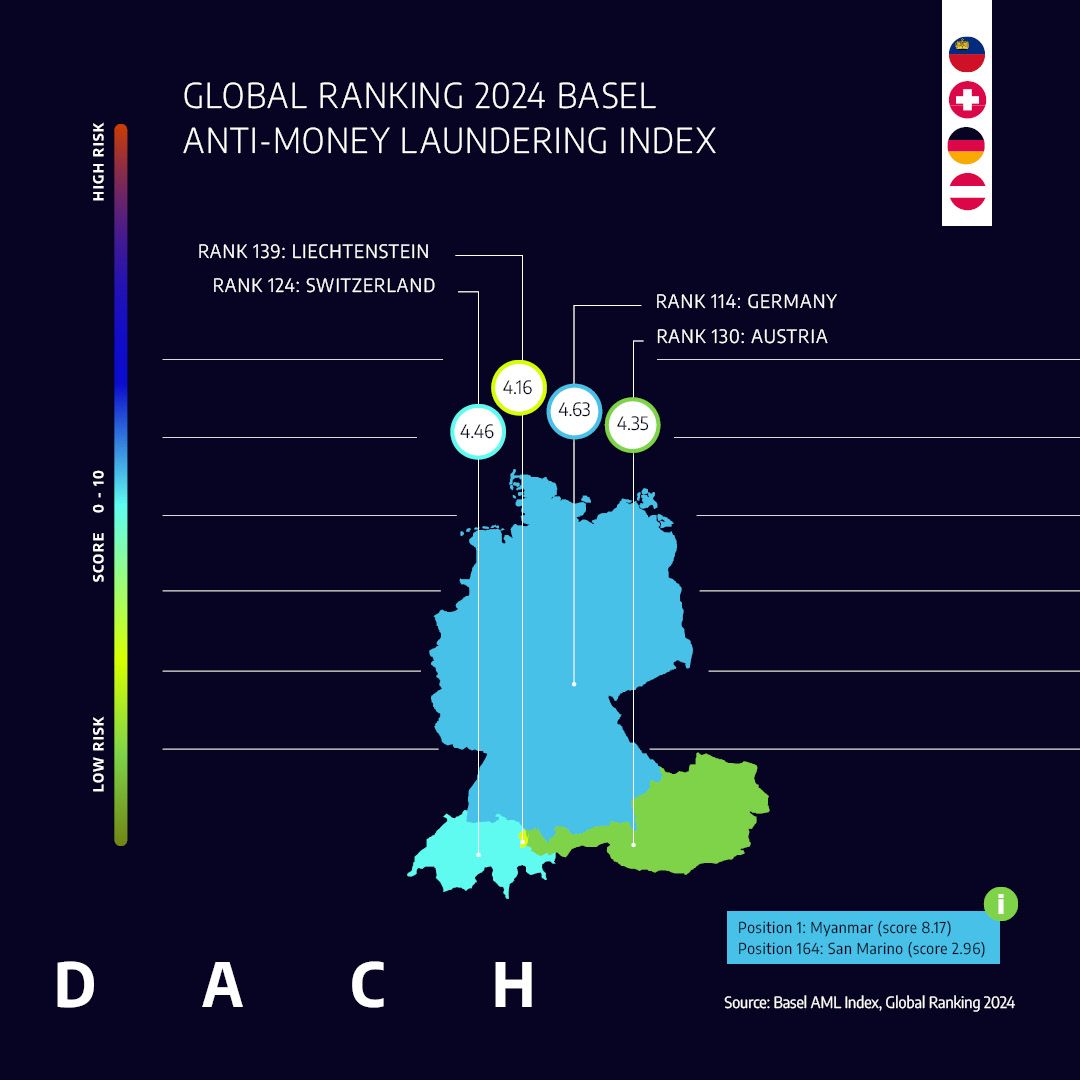

The Basel AML Index measures the risk of money laundering and related financial crimes in countries and jurisdictions around the world. It uses a composite methodology, with 17 indicators in five domains in line with key factors considered to contribute to a high risk.

Out of 164 countries, San Marino received the highest rating in 2024. At the very bottom, in position 164, is Myanmar. Switzerland ranks 124th, while Liechtenstein ranks 139th.

Regardless of the place of business, the following points can be helpful for financial service providers to improve their anti-money laundering activities.

In collaboration with ACTICO, a retail bank rubber-stamped the potential of AI as a means of reducing false positives in the battle against money laundering. The bank used a base of almost 12,000 historical money laundering anomalies to train a machine learning-model to predict which would require further investigation. The model learns from transaction and customer data for which the anomaly was flagged, as well as whether the anomaly required investigation in greater depth to clarify. A validation dataset demonstrated the potential to eliminate around 40 per cent of false positive cases, without overlooking any SAR which would otherwise be notifiable to the financial regulator.

Changes to anti-money laundering laws often plunge banks into extensive adjustment processes. These are not easy to manage, especially given the shortage of human resources.

On top of that, banks are particularly cost-conscious in areas that do not generate revenue. As a result, they are scrutinising their processes more closely and exploring ways to improve efficiency. This also requires a willingness to embrace change.

Machine learning – a component of artificial intelligence – and generative AI (genAI) offer significant potential for cost reduction. High on the priority list are reducing false positives with machine learning and using genAI to support the reporting of suspected money laundering cases to MROS.

You may also be interested in:

News

ACTICO Expands Its Portfolio: Fact Integration Strengthens Market Position

Keensight Capital, one of the leading private equity managers dedicated to pan-European Growth Buyout investments, has acquired a majority stake in the ACTICO Group.

Blog

How Compliance Views AI Agents, LLMs, and Data Sovereignty

Compliance in banking and insurance is embracing AI agents, LLMs, and the cloud, with costs and data sovereignty as key decision factors.

Compliance

AI

Live Event

Shaping the Future of Credit Decisioning – meet ACTICO in Manila

ACTICO joins the Annual Convention of Thrift Banks Philippines 2026 as Silver Sponsor. Discover how thrift banks are automating credit decisions at scale.

Credit Risk Management

Webinar

Webinar: Automated Financial Spreading – The Role of LLMs, Governance, and Audit Trails

Join this 30-minute webinar to understand why orchestrating multiple LLMs falls short on accuracy, auditability, and scale — and see a live demo of purpose-built decisioning AI in action.

Financial Spreading

AI

Newsletter

Regular News and Updates

Decision Management Platform

Compliance

Resources

You are currently viewing a placeholder content from Hubspot Embedded Content. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Hubspot Meetings. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Wistia. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information