News

ACTICO Expands Its Portfolio: Fact Integration Strengthens Market Position

Keensight Capital, one of the leading private equity managers dedicated to pan-European Growth Buyout investments, has acquired a majority stake in the ACTICO Group.

11.01.2022|

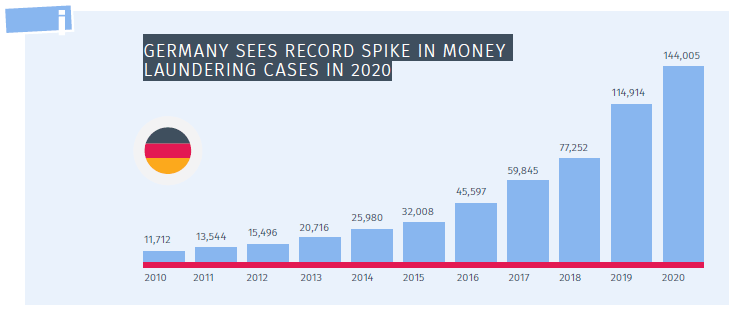

The increase in criminal activity – partly fuelled by the Covid pandemic – is piling the pressure on compliance departments and regulators alike. For example, the volume of suspicious activity reports related to Germany’s Money Laundering Act increased more than twelvefold between 2010 and 2020. The sharp 25% increase in 2020 is also a result of news related to COVID-19 and cryptocurrencies. Other sectors such as notaries also now have to comply in this respect and are required to report transactions linked to money laundering. The FIU in Germany forecasts that the number of SARs will be higher still in 2021.

The situation is similar in other countries: in 2020, the Money Laundering Reporting Office Switzerland (MROS) received more SARs than ever before. The SFIU in Liechtenstein also says volumes are soaring, while the FIU in the Netherlands recorded a 163% increase in the number of suspicious transactions in 2020. It expects the numbers to keep growing, which is why it joined forces with IT specialists and data scientists to set up a DevOps team in 2020.

The financial sector has been flooded with new legislation over the last few years. Key regulations for compliance departments include the EU Money Laundering Directive, the Market Abuse Directive (MAD) and MaRisk compliance. 2020 saw an additional raft of legislation being introduced in Germany, including anti-money laundering regulations based on the all-crimes approach, BaFin’s AUA guidelines relating to the Money Laundering Act, and the European Transparency Register and Financial Information Act (TraFinG). Switzerland has also amended certain legislation, and the revised Money Laundering Act will come into force in 2022. In 2024, the EU’s new Anti-Money Laundering Authority (AMLA) is set to begin work on creating a single integrated system to combat money laundering and terrorist financing. All of this means more work for banks and insurers.

This has all increased the pressure on compliance teams in their fight against money laundering – exacerbated still further by the shortage of skilled staff and rising costs. Banks and insurance companies have already invested massively in compliance, but conventional methods are simply inadequate to tackle the increasingly complex work involved and the growing flood of data. Yet if internal control mechanisms fail to do their job, banks risk incurring massive fines that can run to millions. Banks all around the globe were hard hit by this.

Staff shortages in compliance departments and rising costs are ramping up the pressure on banks and insurers. One step they can take is to reduce false positives, also known as false alarms. Rule-based IT systems generate these reports, which are technically accurate but on closer inspection clearly do not represent a money laundering risk. They place an unnecessary burden on compliance staff because every false positive has to be clarified. Many financial institutions have already tackled this issue and achieved real improvements thanks to machine learning.

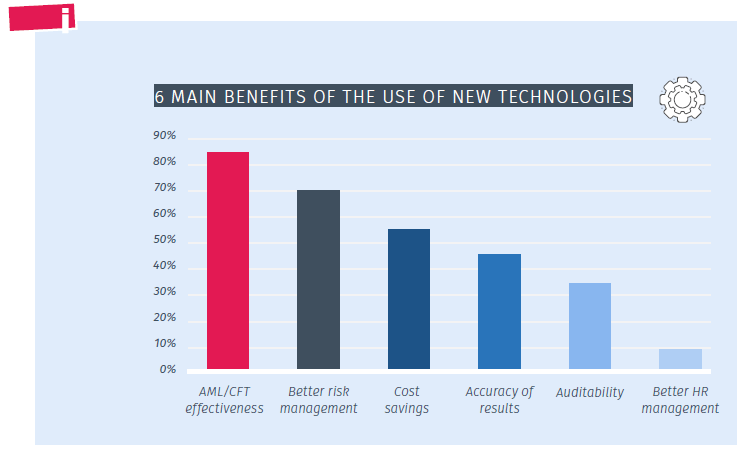

Machine learning – a component of artificial intelligence – analyzes potential money laundering cases based on data knowledge. Supplemented by the knowledge and experience of compliance staff in the specific area, it is possible to identify anomalies with greater speed and efficiency. As a result, huge data volumes can be analyzed more efficiently, suspicious patterns detected more easily, and potential risks identified at an early stage. This is also the conclusion of a recent study by the FATF (Financial Action Task Force on Money Laundering), a leading international body in the fight against money laundering. By using automation and machine learning, compliance departments can reduce the amount of work involved in complex analysis and review, increase efficiency, and cut costs.

Source: FATF: Opportunities and challenges of new technologies for AML/CFT

In practice, banks are shrinking their workload by 50%, for example in payment screening. Another example is PEP and sanctions list screening. Once again, machine learning is helping to reduce hit rates by up to 60%, allowing compliance teams to focus on true positives and allocate their time accordingly.

How many financial transactions can you monitor and clarify daily? Learn how modern software helps banks, insurers and financial services providers ensure AML compliance.

You may also be interested in:

News

ACTICO Expands Its Portfolio: Fact Integration Strengthens Market Position

Keensight Capital, one of the leading private equity managers dedicated to pan-European Growth Buyout investments, has acquired a majority stake in the ACTICO Group.

Blog

How Compliance Views AI Agents, LLMs, and Data Sovereignty

Compliance in banking and insurance is embracing AI agents, LLMs, and the cloud, with costs and data sovereignty as key decision factors.

Compliance

AI

Live Event

Shaping the Future of Credit Decisioning – meet ACTICO in Manila

ACTICO joins the Annual Convention of Thrift Banks Philippines 2026 as Silver Sponsor. Discover how thrift banks are automating credit decisions at scale.

Credit Risk Management

Webinar

Webinar: Automated Financial Spreading – The Role of LLMs, Governance, and Audit Trails

Join this 30-minute webinar to understand why orchestrating multiple LLMs falls short on accuracy, auditability, and scale — and see a live demo of purpose-built decisioning AI in action.

Financial Spreading

AI

Newsletter

Regular News and Updates

Decision Management Platform

Compliance

Resources

You are currently viewing a placeholder content from Hubspot Embedded Content. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from HubSpot. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Hubspot Meetings. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Wistia. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information